一. 前言

Anscombe's quartet, 安斯库姆四重奏.

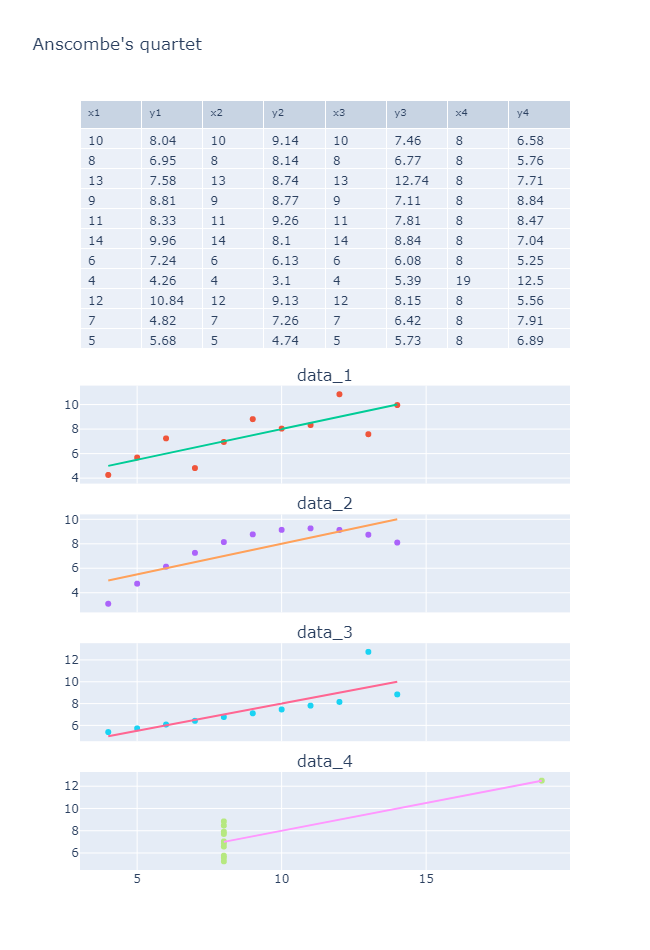

Anscombe's quartet comprises four data sets that have nearly identical simple descriptive statistics, yet have very different distributions and appear very different when graphed. Each dataset consists of eleven (x,y) points. They were constructed in 1973 by the statistician Francis Anscombe to demonstrate both the importance of graphing data when analyzing it, and the effect of outliers and other influential observations on statistical properties. He described the article as being intended to counter the impression among statisticians that "numerical calculations are exact, but graphs are rough."[1]

| I | II | III | IV | ||||

|---|---|---|---|---|---|---|---|

| x | y | x | y | x | y | x | y |

| 10.0 | 8.04 | 10.0 | 9.14 | 10.0 | 7.46 | 8.0 | 6.58 |

| 8.0 | 6.95 | 8.0 | 8.14 | 8.0 | 6.77 | 8.0 | 5.76 |

| 13.0 | 7.58 | 13.0 | 8.74 | 13.0 | 12.74 | 8.0 | 7.71 |

| 9.0 | 8.81 | 9.0 | 8.77 | 9.0 | 7.11 | 8.0 | 8.84 |

| 11.0 | 8.33 | 11.0 | 9.26 | 11.0 | 7.81 | 8.0 | 8.47 |

| 14.0 | 9.96 | 14.0 | 8.10 | 14.0 | 8.84 | 8.0 | 7.04 |

| 6.0 | 7.24 | 6.0 | 6.13 | 6.0 | 6.08 | 8.0 | 5.25 |

| 4.0 | 4.26 | 4.0 | 3.10 | 4.0 | 5.39 | 19.0 | 12.50 |

| 12.0 | 10.84 | 12.0 | 9.13 | 12.0 | 8.15 | 8.0 | 5.56 |

| 7.0 | 4.82 | 7.0 | 7.26 | 7.0 | 6.42 | 8.0 | 7.91 |

| 5.0 | 5.68 | 5.0 | 4.74 | 5.0 | 5.73 | 8.0 | 6.89 |

即四组被精心构造出来的数据, 用于说明异常值对于统计分析的影响, 以及数据可视化对于数据分析的重要性.

二. 问题

2.1 基本信息

from io import StringIO

import pandas as pd

import plotly.express as px

import statsmodels.api as sta

df = pd.read_csv(StringIO(

'''x1,y1,x2,y2,x3,y3,x4,y4

10,8.04,10,9.14,10,7.46,8,6.58

8,6.95,8,8.14,8,6.77,8,5.76

13,7.58,13,8.74,13,12.74,8,7.71

9,8.81,9,8.77,9,7.11,8,8.84

11,8.33,11,9.26,11,7.81,8,8.47

14,9.96,14,8.1,14,8.84,8,7.04

6,7.24,6,6.13,6,6.08,8,5.25

4,4.26,4,3.1,4,5.39,19,12.5

12,10.84,12,9.13,12,8.15,8,5.56

7,4.82,7,7.26,7,6.42,8,7.91

5,5.68,5,4.74,5,5.73,8,6.89

'''

))

df

| x1 | y1 | x2 | y2 | x3 | y3 | x4 | y4 |

|---|---|---|---|---|---|---|---|

| 10 | 8.04 | 10 | 9.14 | 10 | 7.46 | 8 | 6.58 |

| 8 | 6.95 | 8 | 8.14 | 8 | 6.77 | 8 | 5.76 |

| 13 | 7.58 | 13 | 8.74 | 13 | 12.74 | 8 | 7.71 |

| 9 | 8.81 | 9 | 8.77 | 9 | 7.11 | 8 | 8.84 |

| 11 | 8.33 | 11 | 9.26 | 11 | 7.81 | 8 | 8.47 |

| 14 | 9.96 | 14 | 8.10 | 14 | 8.84 | 8 | 7.04 |

| 6 | 7.24 | 6 | 6.13 | 6 | 6.08 | 8 | 5.25 |

| 4 | 4.26 | 4 | 3.10 | 4 | 5.39 | 19 | 12.50 |

| 12 | 10.84 | 12 | 9.13 | 12 | 8.15 | 8 | 5.56 |

| 7 | 4.82 | 7 | 7.26 | 7 | 6.42 | 8 | 7.91 |

| 5 | 5.68 | 5 | 4.74 | 5 | 5.73 | 8 | 6.89 |

df.describe()

| x1 | y1 | x2 | y2 | x3 | y3 | x4 | y4 | |

|---|---|---|---|---|---|---|---|---|

| count | 11.000000 | 11.000000 | 11.000000 | 11.000000 | 11.000000 | 11.000000 | 11.000000 | 11.000000 |

| mean | 9.000000 | 7.500909 | 9.000000 | 7.500909 | 9.000000 | 7.500000 | 9.000000 | 7.500909 |

| std | 3.316625 | 2.031568 | 3.316625 | 2.031657 | 3.316625 | 2.030424 | 3.316625 | 2.030579 |

| min | 4.000000 | 4.260000 | 4.000000 | 3.100000 | 4.000000 | 5.390000 | 8.000000 | 5.250000 |

| 25% | 6.500000 | 6.315000 | 6.500000 | 6.695000 | 6.500000 | 6.250000 | 8.000000 | 6.170000 |

| 50% | 9.000000 | 7.580000 | 9.000000 | 8.140000 | 9.000000 | 7.110000 | 8.000000 | 7.040000 |

| 75% | 11.500000 | 8.570000 | 11.500000 | 8.950000 | 11.500000 | 7.980000 | 8.000000 | 8.190000 |

| max | 14.000000 | 10.840000 | 14.000000 | 9.260000 | 14.000000 | 12.740000 | 19.000000 | 12.500000 |

每组数据x, y的标准差, 均值两项数据值基本相等.

2.2 相关性

for i in range(1, 5):

print(df[[f'x{i}',f'y{i}']].corr())

x1 y1

x1 1.000000 0.816421

y1 0.816421 1.000000

x2 y2

x2 1.000000 0.816237

y2 0.816237 1.000000

x3 y3

x3 1.000000 0.816287

y3 0.816287 1.000000

x4 y4

x4 1.000000 0.816521

y4 0.816521 1.000000

每组数据的相关性系数基本相等, r ≈ 0.816.

2.3 线性拟合

使用statsmodels对数据进行线性拟合.

for i in range(1, 5):

x = sta.add_constant(df[f'x{i}'])

model = sta.OLS(df[f'y{i}'], x).fit()

print(model.summary())

C:\Users\Lian\anaconda3\lib\site-packages\scipy\stats\stats.py:1541: UserWarning: kurtosistest only valid for n>=20

... continuing anyway, n=11

warnings.warn("kurtosistest only valid for n>=20 ... continuing "

OLS Regression Results

==============================================================================

Dep. Variable: y1 R-squared: 0.667

Model: OLS Adj. R-squared: 0.629

Method: Least Squares F-statistic: 17.99

Date: Thu, 27 Apr 2023 Prob (F-statistic): 0.00217

Time: 12:16:11 Log-Likelihood: -16.841

No. Observations: 11 AIC: 37.68

Df Residuals: 9 BIC: 38.48

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 3.0001 1.125 2.667 0.026 0.456 5.544

x1 0.5001 0.118 4.241 0.002 0.233 0.767

==============================================================================

Omnibus: 0.082 Durbin-Watson: 3.212

Prob(Omnibus): 0.960 Jarque-Bera (JB): 0.289

Skew: -0.122 Prob(JB): 0.865

Kurtosis: 2.244 Cond. No. 29.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

C:\Users\Lian\anaconda3\lib\site-packages\scipy\stats\stats.py:1541: UserWarning: kurtosistest only valid for n>=20

... continuing anyway, n=11

warnings.warn("kurtosistest only valid for n>=20 ... continuing "

OLS Regression Results

==============================================================================

Dep. Variable: y2 R-squared: 0.666

Model: OLS Adj. R-squared: 0.629

Method: Least Squares F-statistic: 17.97

Date: Thu, 27 Apr 2023 Prob (F-statistic): 0.00218

Time: 12:16:11 Log-Likelihood: -16.846

No. Observations: 11 AIC: 37.69

Df Residuals: 9 BIC: 38.49

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 3.0009 1.125 2.667 0.026 0.455 5.547

x2 0.5000 0.118 4.239 0.002 0.233 0.767

==============================================================================

Omnibus: 1.594 Durbin-Watson: 2.188

Prob(Omnibus): 0.451 Jarque-Bera (JB): 1.108

Skew: -0.567 Prob(JB): 0.575

Kurtosis: 1.936 Cond. No. 29.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

C:\Users\Lian\anaconda3\lib\site-packages\scipy\stats\stats.py:1541: UserWarning: kurtosistest only valid for n>=20

... continuing anyway, n=11

warnings.warn("kurtosistest only valid for n>=20 ... continuing "

OLS Regression Results

==============================================================================

Dep. Variable: y3 R-squared: 0.666

Model: OLS Adj. R-squared: 0.629

Method: Least Squares F-statistic: 17.97

Date: Thu, 27 Apr 2023 Prob (F-statistic): 0.00218

Time: 12:16:11 Log-Likelihood: -16.838

No. Observations: 11 AIC: 37.68

Df Residuals: 9 BIC: 38.47

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 3.0025 1.124 2.670 0.026 0.459 5.546

x3 0.4997 0.118 4.239 0.002 0.233 0.766

==============================================================================

Omnibus: 19.540 Durbin-Watson: 2.144

Prob(Omnibus): 0.000 Jarque-Bera (JB): 13.478

Kurtosis: 6.571 Cond. No. 29.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

C:\Users\Lian\anaconda3\lib\site-packages\scipy\stats\stats.py:1541: UserWarning: kurtosistest only valid for n>=20

... continuing anyway, n=11

warnings.warn("kurtosistest only valid for n>=20 ... continuing "

OLS Regression Results

==============================================================================

Dep. Variable: y4 R-squared: 0.667

Model: OLS Adj. R-squared: 0.630

Method: Least Squares F-statistic: 18.00

Date: Thu, 27 Apr 2023 Prob (F-statistic): 0.00216

Time: 12:16:11 Log-Likelihood: -16.833

No. Observations: 11 AIC: 37.67

Df Residuals: 9 BIC: 38.46

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 3.0017 1.124 2.671 0.026 0.459 5.544

x4 0.4999 0.118 4.243 0.002 0.233 0.766

==============================================================================

Omnibus: 0.555 Durbin-Watson: 1.662

Prob(Omnibus): 0.758 Jarque-Bera (JB): 0.524

Skew: 0.010 Prob(JB): 0.769

Kurtosis: 1.931 Cond. No. 29.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

>>>

每组数组得到的拟合线性方程, 基本趋于一致, 更重要的是R方(R-squared)也是趋于一致:

再细看每组的拟合结果的检验, 如T值, 置信区间等.

const 3.0001 1.125 2.667 0.026 0.456 5.544

x1 0.5001 0.118 4.241 0.002 0.233 0.767

const 3.0009 1.125 2.667 0.026 0.455 5.547

x2 0.5000 0.118 4.239 0.002 0.233 0.767

const 3.0025 1.124 2.670 0.026 0.459 5.546

x3 0.4997 0.118 4.239 0.002 0.233 0.766

const 3.0017 1.124 2.671 0.026 0.459 5.544

x4 0.4999 0.118 4.243 0.002 0.233 0.766

在数值型数据结果上, 上述的四组数据做到了近乎惊人的多方面一致性.

2.4 数据可视化

for i in range(1, 5):

x = sta.add_constant(df[f'x{i}'])

model = sta.OLS(df[f'y{i}'], x).fit()

# 得到拟合后的值

df[f'fit_{i}'] = model.fittedvalues

# 创建画布

fig = make_subplots(

rows=5,

cols=1,

shared_xaxes=True,

# 间隔

vertical_spacing=0.04,

# 相对高度

row_heights=[780, 300, 300, 300, 300],

# 子图标题

subplot_titles=['', *[f'data_{i}' for i in range(1, 5)]],

# 子图类型, 必须指定, 在绘制table

specs=[[{"type": "table"}],

* [[{"type": "scatter"}]] * 4]

)

fig.add_trace(

go.Table(

header=dict(

values=list(df.columns.values[:8]),

font=dict(size=10),

align="left"

),

cells=dict(

values=[df[k].tolist() for k in df.columns.values[:8]],

align = "left"),

),

col=1,

row=1,

)

for i in range(2, 6):

# 绘制散点图

fig.add_trace(

go.Scatter(

x=df[f'x{i-1}'],

y=df[f"y{i-1}"],

mode="markers",

name=f"data_{i - 1}",

showlegend=False

),

row= i,

col= 1

)

# 绘制拟合直线

fig.add_trace(

go.Scatter(

x=df[f'x{i-1}'],

y=df[f"fit_{i-1}"],

mode="lines",

showlegend=False

),

row= i,

col= 1

)

fig.update_layout(

width= 650,

height=950,

title ="Anscombe's quartet"

)

fig.show()

可以看到, 线性相关拟合的各种数据和实际数据分布之间的巨大差异.

三. 小结

- 数据处理注意离群值.

- 在进行线性(数据)相关分析时, 最好先进行数据可视化, 观察数据的分布情况.

- 皮尔逊相关性分析/线性回归对于异常值非常敏感.